By John Engel

Compass will acquire Anywhere Real Estate in an all-stock deal valued at $1.6 billion, while assuming about $2.6 billion of Anywhere’s debt. The combined enterprise value is about $10 billion. Reported targets include $225-$255 million in annual cost savings and a combined footprint of roughly 100,000 company agents plus 250,000 franchise agents. Nearly one in four U.S. agents will now be under the same roof. (Spoiler alert: not so in New Canaan.)

Anywhere brings the global reach. Its brands — Coldwell Banker, Sotheby’s International Realty, Century 21, ERA, Corcoran, and Better Homes & Gardens — add up to nearly 18,000 offices, 100,000 agents, and another 250,000 franchised associates across 119 countries and territories. Coldwell Banker alone operates in 48 countries. This merger instantly gives Compass international scale it never had and U.S. breadth to spread technology and back-office costs.

Why pay a premium for a company with debt? The answer lies in valuation. Compass has always pitched itself as a technology company. In 2020, it generated $3.7 billion of revenue, lost $270 million, and was still valued at $6.4 billion. Anywhere, by contrast, produced $5.7 billion of revenue last year but carries $2.6 billion of debt. In Q2 2025, it managed $27 million of profit on $1.7 billion of revenue — margins too thin to excite investors, who gave it a book value of only $800 million, a relative steal. Compass reported $2.06 billion that quarter and finally turned cash-flow positive, with $68 million in free cash flow, even while it still posts net losses.

Compass must grow as long as investors continue to buy the growth story built on 97.5% agent retention, 24 logins a week per agent, and a tech platform sticky enough to justify a premium. That is why Compass can pay 84% above Anywhere’s stock price, using shares instead of cash, and convince the Street the math works. That’s why Compass bought @properties and Christie’s International Real Estate earlier this year, and that’s why they unsuccessfully bid $4 per share for Douglas Elliman when the stock was trading around $2.

For Compass, three strategic reasons stand out.

First, domestic share: With nearly 25% of U.S. transactions, Compass has less need to pay costly bonuses and high splits to poach top agents in strategic markets.

Second, international reach: Coldwell Banker’s network alone plants the Compass flag in 48 countries.

Third, efficiency: Compass spends heavily on technology, and spreading those fixed costs across 350,000 agents and layering in $225–$255 million of cost cuts makes the financial model look sustainable.

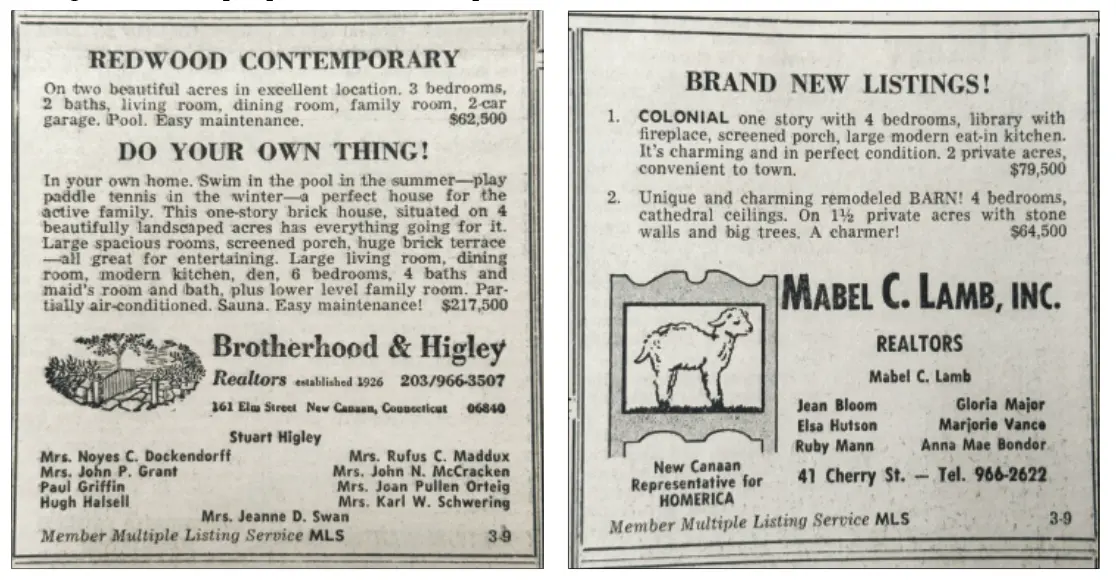

Over the past twenty years, most New Canaan signs changed hands: Barbara Cleary’s Realty Guild γ Halstead (2015) γ Brown Harris Stevens (2020); Brotherhood & Higley γ Kelly Associates γ Houlihan Lawrence (2015; HL later acquired by Berkshire Hathaway’s HomeServices in 2017, name kept); Prudential Connecticut Realty γ Berkshire Hathaway HomeServices (2013); William Pitt Sotheby’s shifted control when BLT bought into the franchise (2008); Mabel Lamb folded into Coldwell Banker.

Today, the market is competitive and fragmented: eight firms with storefronts in a one-square-mile core, none above 20% share. Offices: Compass (111 Cherry St.), Coldwell Banker (170 Main St.), William Pitt Sotheby’s BLT-owned local franchise (26 Cherry St.), Brown Harris Stevens (93 Cherry St.), Douglas Elliman (199 Elm St.), William Raveis (4 Elm St.), and Houlihan Lawrence (161 Elm St.). The Agency maintains an office on South Avenue but didn’t crack the top 25 local firms. By volume, Compass is #4 and Coldwell Banker #6, and together they’ll be ~19% of market share, within two percentage points of William Pitt Sotheby’s, William Raveis, and Houlihan Lawrence. Note: William Pitt Sotheby’s carries the Sotheby’s brand but is independent of the Compass+Anywhere deal due to BLT’s ownership; Brown Harris Stevens and Raveis are family-owned; and Elliman is independent and publicly traded.

Clients have already lived through the shifts. When Cleary’s sign came down, when Brotherhood & Higley sold, when Prudential became Berkshire Hathaway, the brokers remained but the names changed. Each deal promised continuity, yet the landscape tilted more toward regional flags.

Now, the biggest merger in U.S. real estate history lands on Elm Street and Main Street, where buyers and sellers see eight brands with retail storefronts competing for their listing.

Why does the national news matter locally? There are four quick effects to watch.

First, recruiting: If Compass controls both sides of the split wars, the constant churn of agents chasing the richest offer may slow.

Second, office overlaps: The companies have promised $225–$255 million in savings. That usually means fewer back-office roles and fewer storefronts. New Canaan, Darien, and Stamford have multiple overlapping offices, and we’re starting to see the first wave of closures.

Third, international referrals: Compass now controls the Anywhere referral pipeline, which spans 119 countries. That could benefit New Canaan’s relocation and luxury clients.

Fourth, branding: Anywhere owns Coldwell Banker and Sotheby’s International Realty, but the local Sotheby’s office is a franchise. If national strategy shifts, local marketing could follow.

Reaction in the industry was swift. Ryan Serhant, speaking from the back of a car, told agents, “If you woke up today being told you have to wear a jersey you did not choose…” His point was simple: Corporate consolidation makes agents feel like headcount. That line struck a chord because it captures the trade-off: Wall Street values size, but agents value identity and service.

Big mergers change headlines; they don’t sell houses. Real estate isn’t a commodity — this isn’t books or diapers moving through a warehouse. It’s a relationship business built on trust, timing, and judgment. In New Canaan, results come from knowing which buyer is flying in on Friday, which school streets fill first, what a south-facing kitchen is worth in February, and how to price so you get action in week one, not excuses in week six.

What actually wins listings here is human: straight talk on value, a plan for presentation, the contractor list that shows up tomorrow, photography that fits the season, open houses that feel like an invitation, follow-through that doesn’t miss a call at 9 p.m. Technology can help; scale can widen a referral path. But neither meets the appraiser, calms a nervous seller, or rescues a deal after inspection.

So yes, the logo on the sign may change again. The work won’t. New platforms will come, costs will be shaved, brands will reposition. The advantage in New Canaan still goes to the people who show up, tell the truth, solve problems, and stay with the client from first conversation to closing. That’s how this story gets written — one relationship, one listing, one negotiation at a time.

John Engel is a broker on the Engel Team at Douglas Elliman, and he is working on a sale in Easton this week. Beautiful country up there, apple picking and Christmas tree farms. Unfortunately, an accident shut down the Merritt Parkway this morning and many thousands of cars could not get from there to here for hours, a stark reminder of the fragility of the Connecticut commute and the dependence of our communities on the Parkway.